The Mortgage Industry's Dirty Secret: 60% Fail. Here's the Fix.

Key Takeaways

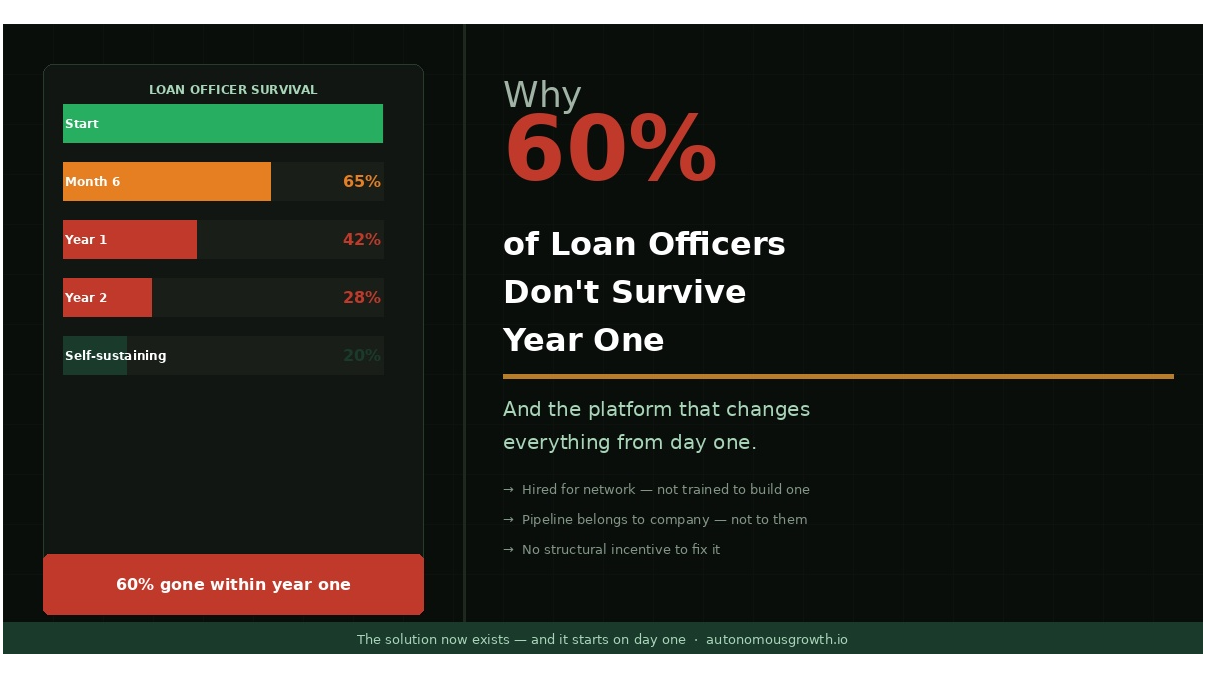

- Between 60% and 80% of new loan officers don't make it through their first year — not because of poor work ethic, but because they were never given the tools to generate leads beyond their initial personal network.

- The average cost to replace a single loan officer is approximately $42,000 — a number that rarely gets discussed loudly enough by the companies absorbing it.

- First-year sales failures across industries consistently trace back to one root cause: a lack of structured prospecting.

- A new shift in how homebuyers search for mortgage help — now increasingly through AI platforms like ChatGPT and Gemini — is quietly rewarding loan officers with a digital presence and penalizing those without one.

- The loan officers who survive past year one aren't necessarily more talented — they have systems that keep working when their personal network runs dry.

The mortgage industry has a quiet crisis on its hands. Every year, thousands of loan officers walk in the door full of energy, armed with contacts, and ready to build something. And every year, most of them are gone before the twelve-month mark. The numbers aren't hidden — they're just not advertised. Understanding why this keeps happening is the first step to breaking the cycle.

60% Gone Before Year Two — The Numbers the Industry Won't Advertise

Some company reports put rookie loan officer turnover between 60% and 80% in the first year alone. Broader industry data shows annual mortgage sector turnover averaging around 25% to 38%, with average loan officer tenure landing somewhere around four years — though the sharpest drop-off happens well before that, in the first twelve months, among the newest cohort, for reasons that have very little to do with talent.

To put that in context: the mortgage industry saw a significant decline in total producing loan officers between 2022 and 2024 — with some estimates pointing to a drop of roughly 46%, though figures vary by source and methodology. That's not just a market slowdown — it's a structural problem playing out in real time. While veteran producers do move companies every few years, the steepest attrition consistently hits new loan officers in their first year.

The industry talks about churn the way it talks about the weather — as something that just happens. But churn at this scale isn't natural. It's the predictable result of a system that was never designed to help new loan officers succeed past the first few months.

The Network Cliff: When Month 6 Becomes Month Last

Hired for a Rolodex, Not a System

The standard loan officer recruiting pitch goes something like this: bring your contacts, bring your realtor relationships, bring your warm market. Companies recruit based on the network a candidate already has — not on whether they have any infrastructure to build new relationships once that network is tapped out.

This matters enormously, because a mortgage is a relationship-driven business. Success depends heavily on trust, referrals, and repeat clients. New loan officers without an established client base are operating on borrowed time from day one. They're depleting their personal network with every deal — and in most cases, nobody has trained them to replace what they're spending.

The result is predictable. A new LO has a strong first two or three months. Their friends are close. Their family refinances. Their former colleagues ask for help. Then the calls slow down. The referrals dry up. And there's no pipeline behind them to pick up the slack.

The Exhaustion Timeline Most LOs Never See Coming

Research across industries shows that roughly one-third of employees quit within their first six months of a new job. In mortgage, that pattern is even more pronounced — and the timing is almost always the same. Month six is when the initial network runs dry. It's when the gap between how many people an LO knows and how many leads they need becomes impossible to ignore.

High first-year LO turnover is frequently attributed to loan officers giving up too early or feeling overwhelmed. But those explanations miss the point. What looks like giving up is often the rational response to an unsolvable math problem: a depleted personal network, no trained replacement system, and mounting pressure to produce. The exhaustion is real — but it's structural, not personal.

Why Failure Isn't About Effort

Never Set Up to Succeed

A consistent finding across workforce research is that a significant share of new employees who leave early report they weren't properly equipped to succeed — citing insufficient training and unclear job expectations as primary drivers. In mortgage specifically, inadequate preparation is widely recognized as a key factor in early loan officer attrition.

This isn't about motivation or attitude. It's about preparation. A new loan officer can be hardworking, personable, and genuinely good at the job — and still fail, because nobody showed them how to build a pipeline from scratch. Product knowledge and compliance training don't fill that gap. Knowing how a rate lock works doesn't generate a single inbound lead.

First-Year Sales Failures Trace Back to Prospecting Gaps

The prospecting problem isn't unique to mortgage. Sales research consistently identifies a lack of structured prospecting as the leading driver of first-year failure across industries. But in mortgage, the stakes are higher — because the sales cycle is long, the client relationships are personal, and there's no reliable foot traffic to fall back on. You can't just open the doors and wait.

Without a structured approach to lead generation, a new LO is essentially playing a numbers game with a shrinking deck of cards. Every contact they reach out to is one fewer left in the pile. And once the pile is gone, most have no idea how to build a new one.

Inconsistent Pipelines, Slow Responses, No Follow-Up Structure

Beyond prospecting, operational gaps compound quickly. Common failure factors include inconsistent pipelines, slow response times, and a total absence of structured follow-up. Cold mortgage leads don't stay warm for long. A borrower who submits an inquiry and waits 24 hours for a callback has already called three other loan officers.

These aren't character flaws. They're the natural result of a single person trying to simultaneously generate leads, manage multiple loan files, maintain realtor relationships, and respond to every inquiry — without any automated support. The workload alone is designed to break someone without systems in place.

Who Actually Benefits From the Revolving Door

Recruiters, Companies, and Lead Vendors Win Every Cycle

It's worth being direct about the incentive structure here — not to assign blame, but because understanding it explains why the problem persists. High loan officer turnover is, financially speaking, good for almost everyone except the loan officer.

Recruiters earn placement fees on every new hire. Mortgage companies benefit from the warm network each recruit brings in the first few months. Lead-generation portals profit by selling pipeline access to new LOs with nothing else to fall back on. Training programs have a constant stream of new students. Tech platforms add new subscribers each cycle. The revolving door keeps all of these wheels turning.

The loan officer, meanwhile, leaves with nothing. Whatever CRM contacts they built, whatever pipeline they developed, whatever digital presence was created — it typically lives on the company's servers, under the company's brand. They start over from zero. The cycle begins again.

The $42,000 Cost Nobody Talks About Loudly Enough

There is one group that genuinely loses in this arrangement: brokers and branch managers. The average cost to replace a single loan officer is approximately $42,000, when accounting for recruiting fees, onboarding time, lost production during ramp-up, and the training investment. That number is widely cited in cost analyses of the mortgage industry — and it's widely absorbed in silence.

Brokers don't talk about it loudly because it implies the system they're running is broken. But the math is hard to argue with. A branch that loses four loan officers in a year has effectively written a $168,000 check to the revolving door. A retention-focused approach — one that actually gives new LOs the infrastructure to survive — isn't just better for the loan officer. It's a significant business opportunity for the people managing them.

The AI Shift That Changes the Equation

Homebuyers Are Searching Through AI — Not Just Google

A shift happening right now that most loan officers aren't fully aware of yet: a growing share of home shoppers now use AI platforms for real estate and mortgage research. Tools like ChatGPT and Gemini are being used by mainstream homebuyers to learn about mortgage basics, run payment calculations, and search for loan officers via conversational AI — rather than traditional search results.

What that means practically is that a loan officer without a presence optimized for AI platforms is invisible to a meaningful portion of their potential clients before the first conversation even begins. The search behavior has shifted — and the loan officers who recognize it early are the ones who will benefit from the compounding visibility it creates.

GEO: The Visibility Layer Most LOs Don't Know They're Missing

Generative Engine Optimization (GEO) is the emerging practice of structuring online content and data so that AI-powered platforms like ChatGPT, Gemini, and Claude cite and recommend a specific business in their responses. It's a natural evolution of local SEO — which itself remains underutilized by most loan officers despite its well-documented compounding returns.

The window to build an early GEO advantage is open right now, precisely because most loan officers haven't heard of it yet. In markets where established loan officers haven't invested in AI visibility, a new entrant who builds GEO authority from day one can outperform competitors with years of traditional search presence — by occupying the specific positions those competitors left unclaimed. Autonomous Growth builds competitor intelligence analysis directly into this process, identifying exactly where dominant local loan officers are weak in AI visibility before building a new LO's presence around those specific gaps.

Build a Pipeline That Belongs to You — Starting Day One

The thread connecting every failure pattern above is the same: new loan officers don't have systems. They have hustle, they have motivation, and they have a shrinking list of people to call. Systems are what turn a first year into a career. Here's what a day-one infrastructure approach actually looks like in practice.

1. A Complete Digital Presence Built Automatically

The foundation starts with ownership. A professional website, a Google Business Profile, and consistent listings across 40+ directories — all built under the loan officer's personal name, not their employer's brand. This matters more than it sounds. When a loan officer changes companies — and statistically, most will — they keep their digital presence, their reviews, and their accumulated search authority. They don't start over.

For new loan officers who have none of this, the barrier used to be real: no website, no profile, no starting point. That barrier no longer has to exist. A fully automated build process means the infrastructure is live from the first week of a career, not the first year.

2. AI Search Visibility Targeted at Your Market's Gaps

Generic visibility isn't the goal — strategic visibility is. The most effective approach starts with a competitive intelligence analysis: identifying which search terms and AI queries the dominant loan officers in a specific local market are not capturing, then building presence around exactly those gaps first.

This is a fundamentally different approach from trying to outrank established players head-on. Instead of competing for positions they've spent years building, a new LO claims the territory they haven't touched — and builds a GEO score that compounds month over month in the specific areas where opportunity exists.

3. 24/7 Lead Engagement Without Lifting a Finger

One of the most cited reasons loan officers lose warm leads is slow response time. A borrower who submits an inquiry at 9 PM on a Friday shouldn't have to wait until Monday morning. AI-powered conversational agents and automated follow-up systems now make it possible to respond to every inbound inquiry within minutes — around the clock, without any manual involvement from the loan officer.

This eliminates one of the most common and preventable pipeline leaks. It also creates a professional first impression that many established loan officers — working manually — simply can't match consistently.

4. A 12-Month Revenue Plan With Real CAC Projections

Guesswork is one of the biggest silent killers of new loan officer pipelines. Without a structured plan, marketing spend becomes reactive — chasing leads here, trying a new platform there, with no clear picture of what it costs to acquire a client or when to expect results.

A competitor-informed 12-month plan — with actual customer acquisition cost (CAC) projections built from real market data — replaces that guesswork with clarity. Knowing in advance what it costs to generate a closed loan, which months to expect the most traction, and which channels are producing results makes it possible to make real business decisions instead of educated guesses.

Surviving LOs Don't Outwork the Market — They Out-System It

The loan officers who make it past year one share a common thread — and it isn't that they worked harder than everyone else. It's that they had systems that kept producing leads after their personal network ran dry. Structured processes, consistent lead generation, and technology running in the background while they focused on the human side of the business.

The network exhaustion cliff is real. Month six is when most new loan officers feel it — the slowdown, the pressure, the growing gap between the leads they need and the contacts they have left. But it doesn't have to be a cliff. With the right infrastructure in place from day one, it becomes a speed bump — something the pipeline handles automatically while the loan officer keeps building.

The data on first-year failure is stark. The reasons behind it are well-documented. And the tools to address it — competitive intelligence, automated digital presence, GEO visibility, 24/7 lead engagement — now exist and can be activated from the very first day of a loan officer's career. The question is no longer whether the solution is available. It's whether a new LO, or the broker recruiting them, will put it in place before month six arrives.

For loan officers ready to stop guessing and start building a pipeline that compounds from day one, Autonomous Growth delivers a free personalized gap analysis and 12-month marketing plan built specifically for local loan officers and mortgage brokers across the US.

Autonomous Growth ( part of RReputatioNN )

City: Rijkevorsel

Address: 109 Sint-Lenaartsesteenweg #1

Website: https://autonomousgrowth.io

Comments

Post a Comment