When to Secure Financing for Renovations? Real Estate Agent Reveals Timing

Key Takeaways

- Apply for renovation financing 1-4 months before starting work to allow adequate time for approval and avoid project delays

- Market conditions like interest rates and seasonal patterns significantly impact loan terms and approval speed

- HELOCs offer flexibility but require planning, while cash-out refinancing works best during low-rate periods

- Credit score optimization and detailed project estimates help secure favorable financing terms

- DMV area homeowners can maximize ROI by timing renovations strategically before listing properties

Smart homeowners understand that renovation financing requires advance planning. The timing of when you secure funding can make the difference between a smooth project completion and costly delays that drain your budget. Getting this decision right requires understanding market conditions, preparation strategies, and how different loan types align with your renovation timeline.

Why Most Homeowners Time Their Renovation Financing Wrong

The biggest mistake homeowners make is waiting until they're ready to break ground before applying for financing. This reactive approach leads to rushed decisions, limited loan options, and potentially higher costs. Many homeowners assume they can secure funding quickly, but the reality is more complex.

Lenders require detailed project scope documentation, contractor estimates, and thorough financial reviews before approving renovation loans. The approval and underwriting process for many equity-based renovation loans typically takes 30-60 days, though timelines can vary significantly by loan type and lender. Personal loans may process faster, sometimes within days, while home equity loans can take up to six weeks.

Another common timing error occurs when homeowners apply during peak construction seasons without considering how market demand affects both contractor availability and lending capacity. Spring and summer applications often face longer processing times due to increased volume, making early planning even more critical.

Market Conditions That Determine Your Financing Window

Interest Rate Cycles and Lock-In Strategies

Interest rate environments heavily influence when to secure renovation financing. During periods of rising rates, locking in financing early protects against future increases. Most lenders offer rate locks for 30-60 days, with some extending to 90 days for larger projects.

Monitor Federal Reserve announcements and economic indicators that signal rate changes. When rates are trending upward, applying well before your planned start date helps maximize your lock-in window. Conversely, if rates are falling, you might benefit from waiting closer to your project timeline.

Home Equity Requirements for Better Terms

Home equity levels directly impact loan terms and interest rates. For cash-out refinances, many lenders require maintaining at least 20% equity after the loan, meaning you can typically borrow up to 80% of your home's value. Some lenders may allow up to 90% in certain cases. For HELOCs, lenders generally allow borrowing up to a certain loan-to-value ratio, often around 80-90%.

Property values in many markets have increased homeowner equity over time. Current property values may create favorable conditions for equity-based renovation financing, but this advantage requires proper documentation through recent appraisals.

Seasonal Market Patterns That Affect Approval Speed

Loan processing speeds fluctuate seasonally due to application volume. Winter months typically offer faster processing, while spring and summer applications face longer wait times. Plan your financing application during lower-volume periods for quicker approvals.

Additionally, appraisal scheduling affects timelines significantly. Winter applications may benefit from faster appraisal scheduling, potentially reducing overall processing time compared to peak season applications.

Financial Preparations Before Applying

Credit Score and Debt-to-Income Optimization

Credit preparation should begin several months before your financing application. Focus on paying down existing debt, avoiding new credit inquiries, and correcting any errors on credit reports. Even small credit score improvements can reduce interest rates significantly on renovation loans.

Debt-to-income ratios become crucial during renovation financing reviews. Lenders typically want to see ratios below 43% including the new loan payment, though some may accept up to 50% depending on the lender and loan type. Calculate your projected ratio including renovation loan payments before applying to avoid surprises during underwriting.

Detailed Project Scope and Contractor Estimates

Lenders require detailed project documentation including contractor estimates, architectural plans for major renovations, and timeline projections. Gather these documents well before your planned application to ensure accuracy and completeness.

Multiple contractor estimates strengthen your application and help establish realistic project costs. Include 10-15% contingency funds in your financing request to cover unexpected issues that commonly arise during renovation projects.

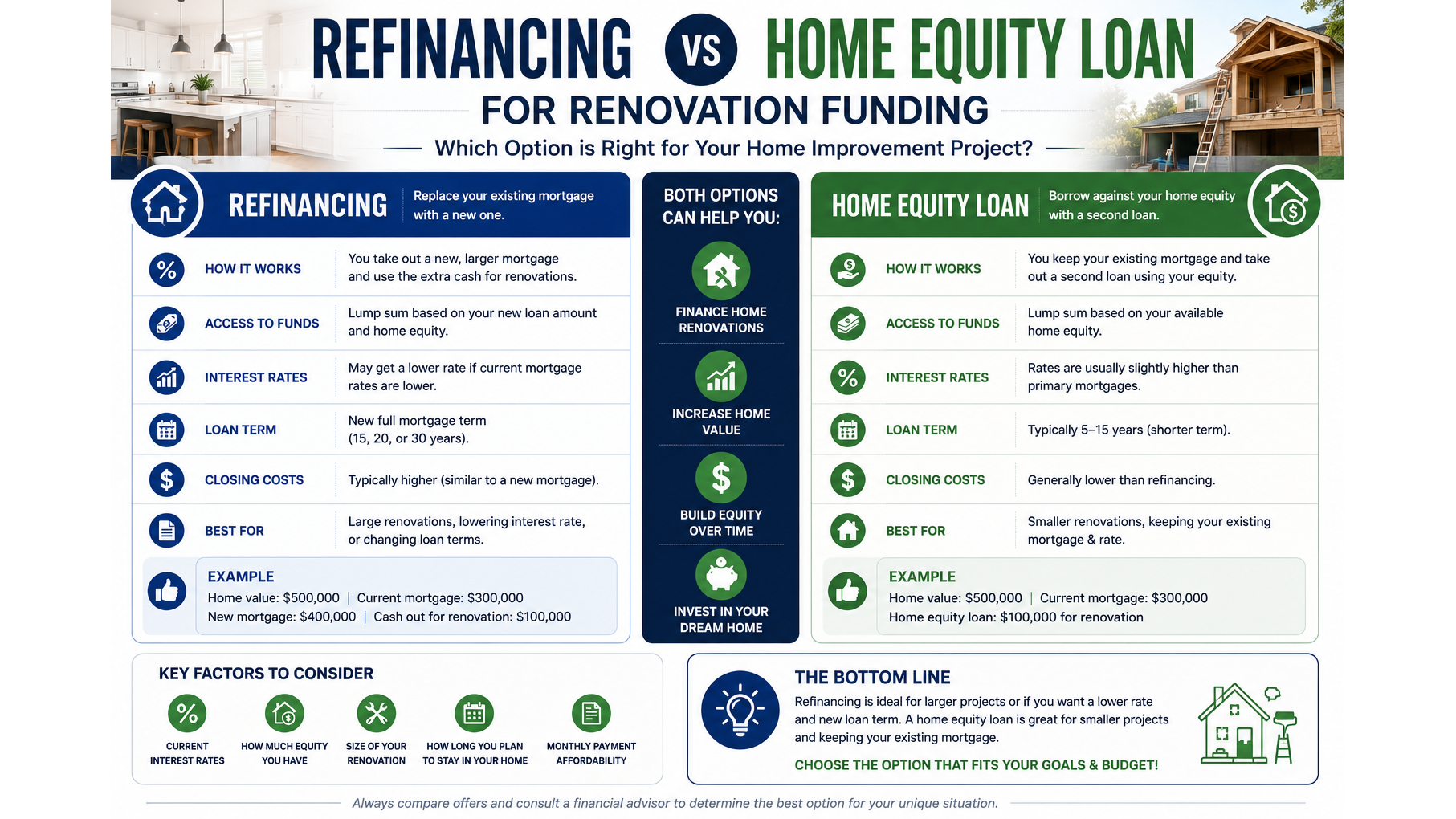

Choosing the Right Financing Type for Your Timeline

Home Equity Lines of Credit (HELOC) Timing

HELOCs offer maximum flexibility for renovation projects with uncertain timelines or phased construction. The draw period typically lasts 10 years, allowing you to access funds as needed. Apply for HELOCs well before your first planned draw to complete the approval and setup process, as approval timelines can vary from a few weeks to a month or more.

Interest rates on HELOCs are variable, making them sensitive to market conditions. Secure HELOC approval when rates are favorable, even if your project timeline extends further out. Most HELOCs don't require immediate fund usage once approved.

Cash-Out Refinance Strategic Windows

Cash-out refinancing works best when current mortgage rates are comparable to or lower than your existing rate. This financing type typically takes 30-45 days to process, with some cases extending to 60 days, making early application important for time-sensitive projects.

Consider cash-out refinancing when you can improve your overall borrowing position by consolidating higher-rate debt or reducing monthly payments while funding renovations. This strategy works particularly well for homeowners with older mortgages at higher rates.

Traditional Home Improvement Loan Considerations

Personal home improvement loans offer faster processing but higher interest rates compared to equity-based options. These loans work well for smaller projects under $50,000 where equity access isn't necessary or practical.

Processing times for personal improvement loans typically range from 7-30 days, with some approving and funding within days. Apply with adequate time before your project start date to allow for fund disbursement and contractor scheduling.

Pre-Sale Renovation Strategy: Maximizing Property Value

ROI Analysis for Local Markets

Many markets show positive returns on kitchen and bathroom renovations. However, financing costs can significantly impact net returns, making timing crucial for pre-sale renovations. Research local market data for renovation ROI in your specific area.

Calculate total financing costs including interest over your expected sale timeline before committing to pre-sale renovation financing. Projects completed within shorter timeframes typically provide better net returns due to reduced interest expenses.

Completion Timeline Before Listing

Plan renovation completion 30-60 days before your intended listing date to allow for final inspections, touch-ups, and professional photography. This timeline also provides buffer for unexpected delays that commonly occur in renovation projects.

Coordinate with your real estate agent early in the planning process to ensure renovations align with market timing and buyer preferences. Understanding seasonal market patterns in your area can help optimize listing timing.

Plan for Renovation Financing 1-4 Months Before Breaking Ground

The optimal financing timeline begins 1-4 months before your planned construction start date. This window allows adequate time for loan shopping, application processing, and rate lock strategies while ensuring funds are available when contractors are ready to begin.

A proactive approach involves starting your financing research several months out, submitting applications 2-3 months before breaking ground, and maintaining buffers for unexpected delays. This timeline accommodates most loan types while providing flexibility for rate timing and contractor scheduling.

Remember that renovation projects often face delays due to permit issues, material availability, or contractor scheduling conflicts. Early financing approval provides peace of mind and negotiating power with contractors who prefer working with clients who have confirmed funding in place.

For guidance on timing your renovation financing with your real estate goals, consult with qualified real estate professionals who understand how renovation investments impact property values in your local market.

Regina Parker, Weichert Real Estate Agent

City: Bowie

Address: 4201 Mitchellville Rd, Suite 203

Website: https://www.myagentregina.com/

Comments

Post a Comment