7 Ways DFW Families Pay for Memory Care Without Insurance or Savings

Key Takeaways

- Memory care costs in Dallas-Fort Worth range from $3,800 to $14,200 monthly, with most families needing multiple funding sources to cover these expenses.

- Texas Medicaid STAR+PLUS waiver programs cover memory care services but not room and board, requiring families to meet strict income limits of $2,982 for singles in 2026.

- VA Aid & Attendance benefits can provide up to $2,424 monthly for qualifying veterans, while selling your parent's home may offer the largest funding source but requires careful tax planning.

- Life insurance settlements and strategic timing of asset liquidation can bridge funding gaps during the transition to long-term care.

- DFW families have access to free guidance through Area Agencies on Aging and elder law attorneys who specialize in Medicaid planning strategies.

When families face the reality that their loved one needs memory care but lack the immediate funds to pay for it, the situation can feel overwhelming. The good news is that multiple funding strategies exist specifically for Dallas-Fort Worth families, often involving a combination of government benefits, asset liquidation, and creative financial planning.

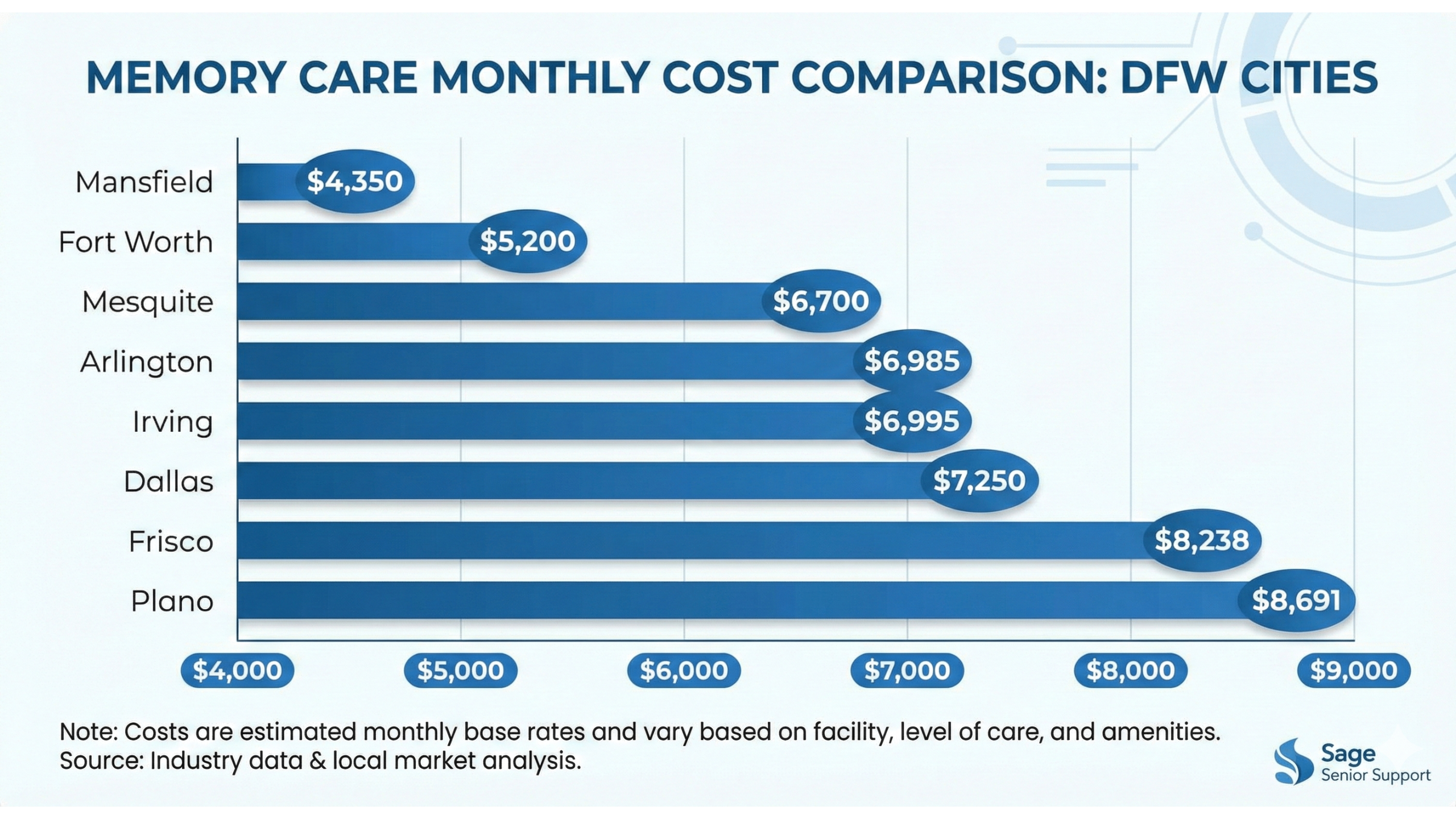

Memory Care Costs $3,800-$14,200 Monthly in DFW

Memory care facilities in the Dallas-Fort Worth metroplex charge significantly different rates depending on location and level of service. In Dallas proper, families can expect to pay around $5,244 monthly, while suburbs like Southlake average $5,831. More affordable options exist in areas like Carrollton at $5,525 monthly or Mansfield at $4,827.

These costs typically include room and board, three meals daily, laundry services, and specialized dementia programming. However, many facilities charge additional "level of care" fees for residents requiring help with medication management, incontinence care, or physical transfers. These add-ons can push a base rate of $6,000 to over $8,000 monthly.

Beyond monthly fees, most DFW memory care facilities require a community fee or move-in fee ranging from $1,000 to $5,000. Sage Senior Support helps families navigate these complex costs by facilitating home sales and connecting them with funding resources throughout the transition process. The reality is that Social Security benefits, averaging $2,071 monthly, cover approximately 40% of typical memory care costs in the region.

Texas Medicaid Programs That Pay for Memory Care

Texas operates two primary Medicaid pathways for memory care funding, each with distinct advantages and limitations. Understanding these programs early in the planning process can mean the difference between affordable care and financial catastrophe.

STAR+PLUS Waiver Covers Services, Not Room and Board

The STAR+PLUS Home and Community-Based Services waiver allows Medicaid to pay for memory care services in assisted living facilities, but it comes with a crucial limitation. Unlike nursing home Medicaid, which covers both services and room and board, the waiver only pays for the care services portion. Residents must still pay for room and board using their Social Security, pension, or other income.

This program operates on a slot system with approximately 24,000 available positions statewide. Once these slots fill up, additional applicants join an interest list that can stretch for months or even years. Families should apply immediately upon receiving a dementia diagnosis, as eligibility isn't determined until a slot becomes available.

2026 Income Limits: $2,982 Single, $5,964 Married

Medicaid eligibility requires meeting strict financial criteria that are updated annually. For 2026, single applicants can have monthly gross income up to $2,982 and countable assets limited to $2,000. Married couples where both spouses are applying face income limits of $5,964 monthly and asset limits of $3,000.

When an individual's income exceeds these limits, Texas allows the creation of a Qualified Income Trust, also called a Miller Trust. This legal instrument enables applicants to "divert" excess income into the trust, making them eligible for Medicaid while ensuring the funds go toward their care costs.

Protecting Your Home from Medicaid Recovery

The family home typically remains an exempt asset during the Medicaid recipient's lifetime, provided it meets certain equity limits ($730,000 for single applicants in 2026). However, Texas operates a Medicaid Estate Recovery Program that can place claims against the estate after death to recover care costs paid by the state.

Families can protect the home through legal instruments like Lady Bird Deeds (Enhanced Life Estate Deeds) or Transfer on Death Deeds. These tools transfer property ownership outside of probate, and since Texas currently only targets probate assets for recovery, the home often remains protected for heirs.

VA Aid & Attendance Benefits for Veterans and Spouses

Veterans and their surviving spouses have access to a valuable but underutilized benefit that can provide substantial financial assistance for memory care costs.

Eligibility Requirements and Maximum Benefit Rates

To qualify, veterans must have served at least 90 days of active duty with at least one day during a recognized wartime period. The veteran doesn't need combat experience or service-connected disabilities. Medically, applicants must require assistance with activities of daily living, which virtually all memory care residents meet.

The 2026 maximum monthly benefits are significant: $2,424 for single veterans, $2,874 for married veterans, and $1,558 for surviving spouses. These tax-free payments are added to the veteran's pension and can substantially offset memory care costs.

How Memory Care Costs Reduce Your Countable Income

The VA uses a net worth limit of $163,699 for eligibility through November 2026. Critically, unreimbursed medical expenses—including the full cost of memory care—are deducted from the applicant's income for calculation purposes. A veteran with $6,000 monthly income but $7,000 in monthly care costs may effectively have zero countable income for benefit purposes.

The application process typically takes four to six months, but benefits are retroactive to the first day of the month following application receipt. Despite this program's value, fewer than one-third of eligible veterans currently receive these benefits.

Selling Your Parent's Home: Timing Is Everything

For most DFW families, home equity represents the largest available asset to fund memory care. However, the timing and method of sale carry significant tax and Medicaid implications that require careful planning.

Capital Gains vs. Stepped-Up Basis at Inheritance

The decision to sell a home during the parent's lifetime versus after death can create dramatic tax differences. When parents gift homes to children while alive, the children inherit the original purchase price as their cost basis. If they later sell, they owe capital gains taxes on decades of appreciation.

Conversely, inherited homes receive a "stepped-up basis" to fair market value at the time of death, potentially eliminating capital gains taxes entirely. In DFW's high-growth market, where homes purchased for $50,000 in 1980 might sell for $450,000 today, this tax difference can exceed $60,000.

Cash Sales for Immediate Funding

Traditional home sales in the DFW market can take 90 days or longer from listing to closing. For families paying $6,500 monthly for memory care, a four-month wait represents $26,000 in out-of-pocket costs. Cash sales to investors can close in 7-10 days, albeit at lower sale prices than traditional market sales.

The trade-off between speed and price depends on the family's immediate cash needs and their ability to cover care costs during a traditional sale process.

Financial Bridge Solutions During Home Sale Process

Bridge loans offer an alternative solution for families who want to pursue a traditional sale while accessing funds immediately. These short-term loans are specifically designed for seniors moving into care, providing funds that "bridge" the gap until home sales complete or other benefits begin.

Some bridge loan products can be approved within 24 hours with no upfront costs, making them valuable tools for families facing immediate care needs while waiting for asset liquidation.

Life Insurance Settlements Provide Immediate Cash

Life insurance policies often represent overlooked assets that can be converted to immediate cash for memory care funding.

Viatical Settlements for Terminal or Chronic Illness

Viatical settlements allow individuals with chronic or terminal illnesses, including advanced Alzheimer's disease, to sell their life insurance policies for immediate cash. Because of shortened life expectancy, these settlements typically pay 50% to 80% of the policy's face value—significantly more than cash surrender values.

Life settlements for healthier individuals over 65 generally provide 3 to 7 times more than cash surrender values, though less than viatical settlements. The key is working with reputable settlement companies that provide competitive bidding processes.

Tax Advantages Under IRS Guidelines for Qualifying Conditions

Viatical settlement proceeds are typically tax-free under IRS guidelines when the insured has a chronic illness requiring long-term care. This tax advantage, combined with the higher payout compared to surrender values, makes life settlements particularly valuable for memory care funding.

Texas has passed specific laws promoting the use of life settlements in Medicaid planning, allowing applicants to sell policies and use proceeds for care without disqualifying them from benefits under certain conditions.

DFW Resources That Provide Free Guidance

North Texas offers several specialized resources to help families navigate memory care funding challenges without cost.

Area Agencies on Aging Benefits Counseling

The Area Agencies on Aging in Dallas and Tarrant Counties provide free benefits counseling to help families understand transitions from Medicare to Medicaid. These agencies offer care coordination, legal assistance referrals, and specialized veteran benefits counseling.

The Dallas County AAA and Tarrant County AAA both maintain ombudsman programs and caregiver support services. The Aging and Disability Resource Center of Tarrant County provides information and assistance for long-term care planning, and may offer guidance on related needs such as housing.

Elder Law Attorneys for Medicaid Planning

Elder law attorneys in the DFW area specialize in "Medicaid Planning," using legal tools like irrevocable trusts to move assets out of parents' names five years before care is needed. They also create Qualified Income Trusts to solve over-income problems and implement Lady Bird Deeds to protect homes from Medicaid Estate Recovery.

These attorneys understand Texas-specific regulations and can coordinate with families' existing financial advisors to create funding strategies. Many offer initial consultations to assess family situations and recommend appropriate planning approaches.

Sage Senior Support Helps DFW Families Navigate Memory Care Funding Through Home Sales

When families need to liquidate their parent's home quickly to fund memory care, having an experienced partner makes all the difference. Understanding both the emotional weight of selling a family home and the financial pressures of immediate care needs requires specialized expertise in the senior care transition process.

The key is finding professionals who understand not just real estate transactions, but the complex interplay between home sales, Medicaid planning, tax implications, and family dynamics. Successful memory care funding often requires coordinating multiple strategies simultaneously—from initiating benefit applications to timing asset sales for optimal tax treatment.

Families benefit most when working with advisors who can explain how home sale proceeds affect Medicaid eligibility, coordinate with elder law attorneys for asset protection, and provide realistic timelines for both traditional and expedited sale processes. This integrated approach ensures that families maximize their resources while maintaining eligibility for government benefits.

Visit Sage Senior Support to learn how their team helps Dallas-Fort Worth families sell homes quickly while managing the complex financial aspects of memory care transitions.

Sage Senior Support

City: Grapevine

Address: 1452 Hughes Rd

Website: https://sageseniorsupport.com

Comments

Post a Comment